Introduction

How to Boost Your Credit Score? Imagine this: a few simple tweaks to your daily financial habits could skyrocket your credit score by over 100 points. Your credit score is not just a random number it is a key that unlocks opportunities like affordable loans, rental approvals, and even certain job offers. A strong score can save you thousands in interest and open doors to better financial deals.

Sadly, many people unknowingly tank their scores with habits like skipping payments, maxing out credit cards, or applying for too many accounts at once. The silver lining? You can turn things around sometimes in just a few months. Ready to take charge of your financial future? Here is your guide to boosting your credit score, step by step.

Section 1: What Exactly Is a Credit Score?

Your credit score is a three digit snapshot of your financial reliability. Lenders use it to decide if you are a safe bet for loans or credit cards. The higher the number, the better your chances of snagging favorable terms like lower interest rates or higher credit limits.

Think of it as your financial report card. It is based on your past behavior with money how you have handled debt, paid bills, and managed credit. Understanding how it works is the first step to mastering it. Ready to dig deeper? Let’s bust some myths and uncover the truth.

Section 2: Busting Credit Score Myths

Misinformation about credit scores is everywhere, and believing the wrong advice can sabotage your efforts. Let’s clear up a couple of big misconceptions right now.

First, there is the myth that checking your own credit score hurts it. Not true! Pulling your own report or using free monitoring tools (like those offered by many banks) is a “soft inquiry” and were not ding your score. In fact, keeping tabs on your credit is smart—it helps you spot errors or fraud early.

Another common tale? Closing old credit accounts boosts your score. Actually, this can backfire. Shutting down accounts shrinks your available credit, which can spike your credit utilization ratio a fancy term for how much of your credit you’re using. A higher ratio can drag your score down, so think twice before canceling that old card. If you want to read more about busting credit score myths click on the link Plus 12 other common credit score myths debunked

Section 3: Simple Tricks to Raise Your Credit Score

Boosting your credit score does not have to be complicated. With a little effort, you can see real progress. Here are two game changers to start with:

- Pay on Time, Every Time: Late payments are a credit score killer. Even one missed due date can leave a mark for years. Set up auto payments or calendar alerts to stay on track.

- Lower Your Credit Utilization: This is the percentage of your available credit you are using. Aim to keep it under 30%. For example, if your card has a $10,000 limit, try not to carry a balance over $3,000. Pay down debt or ask for a higher limit to make this easier.

Small changes like these can add up fast. Let’s explore more ways to build on this momentum.

Section 4: Long Term Habits for a Stellar Score

Improving your credit is not a quick fix it is a lifestyle. Focus on these habits to see lasting gains:

- Mix Up Your Credit: Lenders like to see you can handle different types of credit, like a car loan, a credit card, or a mortgage. Do not overdo it only take on what you can manage but a healthy variety can nudge your score up.

- Keep Old Accounts Open: The length of your credit history matters. That dusty card from 10 years ago? It is proof you have been responsible for a while. Keep it active with small, paid off purchases to preserve your history.

Consistency is key. Stick with these habits, and your score will thank you.

Section 5: More Myths to Toss Out

Let’s debunk a couple more credit score fables that trip people up:

- Carrying a Balance Helps: Nope! You do not need to owe money to build credit. Paying off your cards in full each month shows you’re in control and it saves you interest.

- Income Boosts Your Score: Your paycheck does not factor into your score. What matters is how you manage what you owe, not how much you earn.

Cutting through the noise helps you focus on what actually works. Let’s look at the facts next.

Section 6: Credit Score Basics You Need to Know

Here is the lowdown on how your score comes together:

- It is built from data in your credit report things like payment history, debt levels, and how long you have had credit.

- The two big players in scoring are FICO and VantageScore. Both range from 300 to 850, but they weigh factors slightly differently. Most lenders use FICO, so it is worth getting familiar with.

Knowing what is behind the curtain empowers you to make smarter moves. Let’s get to some actionable tips.

Section 7: Top Tips to Supercharge Your Score

Ready to take your credit score to the next level? Try these:

- Stay Punctual: A flawless payment history is gold. Automate bills or set reminders—whatever keeps you on time.

- Chip Away at Debt: Lower those balances to shrink your credit utilization. Even small payments can help.

- Check Your Reports: Pull your free annual credit reports from AnnualCreditReport.com. Dispute any mistakes you find errors can drag your score down unfairly.

These steps are not flashy, but they work. Let’s break down what drives your score even further.

Section 8: What Really Moves the Needle

Your credit score is not random it is a recipe with specific ingredients. Here are the big ones:

- Payment History (35%): This is the heavyweight. Pay late, and it stings. Pay on time, and you’re golden.

- Credit Utilization (30%): Keep your balances low compared to your limits. It’s a quick way to look responsible.

- Length of History (15%): Older accounts boost your credibility.

- New Credit (10%): Too many applications in a short time can spook lenders.

- Credit Mix (10%): A blend of credit types shows you can juggle different debts.

Focus on the top two they pack the biggest punch.

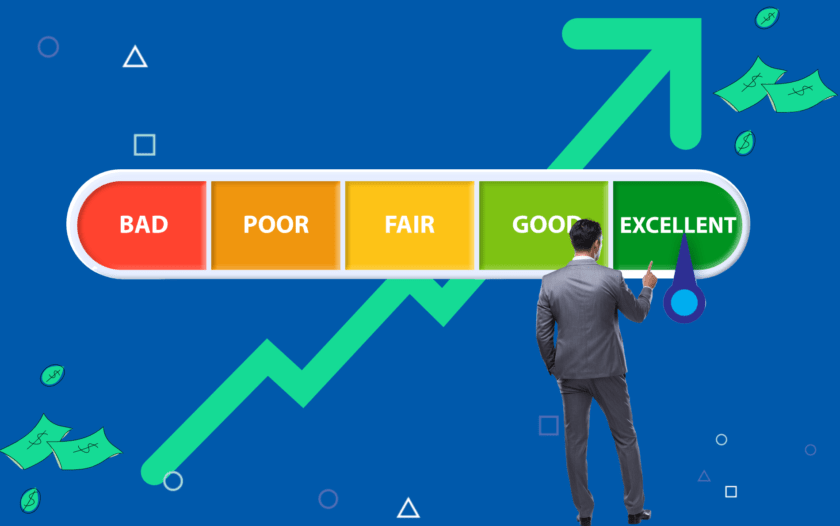

Section 9: Where Does Your Score Stand?

Credit scores run from 300 to 850. Here is the breakdown:

- 800-850: Elite status lenders love you.

- 700-799: Solid ground you will get good offers.

- 650-699: Fair, but room to grow.

- Below 650: Risky territory tougher terms ahead.

Check your score through your bank or a free service like Credit Karma. Knowing your starting point helps you set a target.

Section 10: Why Monitoring Matters

Keeping an eye on your credit is not just for nerds it is a power move. Regular checks let you:

- Catch mistakes or fraud fast.

- Track your progress as you improve.

- Plan your next financial step with confidence.

Sign up for alerts from your bank or a monitoring app. It is like a security system for your finances.

Next to read:

Types of Finance Charges in Different Countries

How to Invest Smartly: A Beginner’s Guide to Growing Wealth

Final Thoughts

Your credit score is more than a number it is a tool for building the life you want. By understanding how it works, ditching the myths, and sticking to smart habits, you can boost your score and unlock better opportunities. Start today with one small step pay a bill on time, check your report, or pay down a card. The results will follow.